Modern payment options abound and pose significant threat to the legacy banking systems. For the mobile payments, Juniper Research estimates that the combined market share of Apple Pay, Samsung Pay, and Google Pay will reach 56% by 2021 in the US. See how custom software developers help banks compete amid changing business landscape.

written by:

Alexander Arabey

Director of Business Development, Partner

![]()

Modern payment options abound and pose significant threat to the legacy banking systems. For the mobile payments, Juniper Research estimates that the combined market share of Apple Pay, Samsung Pay, and Google Pay will reach 56% by 2021 in the US. See how custom software developers help banks compete amid changing business landscape.

How it all started

The history of banking starts as early as 2000 BC in Assyria, where the first premature banking system saw the light. First ‘banking transactions’ had the form of grain loans that merchants gave to farmers and traders carrying goods from city to city. Greek and Roman lenders living approximately that time, based in temples and made loans, accepted deposits and exchanged money. However, it wasn’t until the Medieval and Renaissance periods in Italy that the banking system started to acquire the traits we are familiar with. Particularly affluent cities such as Florence, Venice and Genoa were the fertile ground for the rise and strengthening of the banking industry. By the way, Banca Monte dei Paschi di Siena, headquartered in Siena, Italy, has been continuously operating ever since that time, namely 1472.

How it evolved

By now, banking industry has evolved into a powerful and nearly awe-inspiring industry vertical providing high-demand services. Among these are: consumer banking, global wealth and investment management, global banking and markets, checking and savings accounts, loans, wealth management…the list can be prolonged and will take time to accomplish. Loans alone issued by Wells Fargo totaled $949 bn according to the 2016’s data, while the revenue the bank generated for the same year summed up to $88.2 bn.

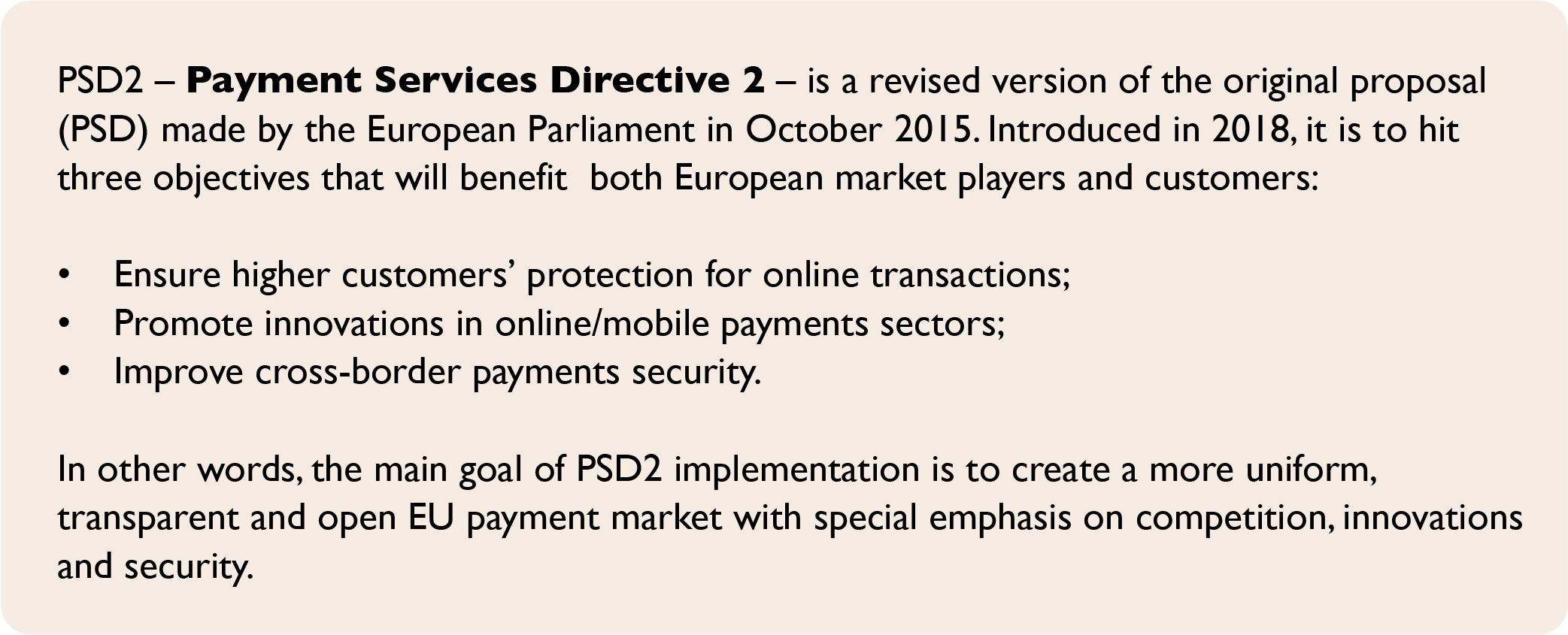

Until recently, alongside the above mentioned service lines, banks fully dominated money transfer and payment sectors as well. Yet, the prevalence of the banking institutions has been significantly shaken since European Union PSD2 directive came into force.

The above mentioned directive made sharing customer account data with merchants, processing companies and the like obligatory for the banks. That being said, BigTechs, mobile operators and fintech companies will now gain access to the bank accounts info and make truly lucrative offers.

Truth be told, the PSD2 implementation was nothing but logical. The shift towards payments decentralization has already become a global trend as can be seen from the cases below.

Mobile wallets

It’s been a while since Apple launched the first mobile payment app in 2014, followed by Samsung and Android in 2015. What started small is projected to total $14 tr by 2022, as mobile payments have gained incredible momentum due to their convenience, transparency and low cost. According to Merchant Machine, estimated 47% of phone users in China have mobile wallets; the Norwegians are almost as interested in paying with their mobile wallets (42%), with the UK (24%) lagging far behind but still boasting impressive figures.

SMS payments

Although more advanced methods of mobile payment have seen a higher growth recently, SMS payments brought remarkable value for the Sub-Saharan Africa users. M-Pesa, Kenya’s largest mobile operator, launched an SMS-based payment system in 2007. As users don’t have to open bank accounts or present credit history, the option drew tremendous number of new customers. M-Pesa saw a particular demand from low-income population living in rural areas without access to regular banking facilities. The mobile operator later evolved to provide an extensive range of services which originally were banking prerogative: loans, money withdrawal and international transfers. As a result, standards of living in rural Kenya improved due to more efficient money transfer among the Kenyan population. Secondly, theft rates reduced as the citizens don’t need to carry cash on them anymore. One more benefit for M-Pesa’s users: small amounts that are saved from using add up to larger savings. As of 2016, M-Pesa’s coverage was 20 million Kenyans which is actually 40% of total country’s population.

QR code payments

In 2014, Adobe Systems conducted a survey in which Germany, France, UK and the US were the participants. The survey was to give the details on how frequently the QR code is used. At that time, it showed that 25-30% of the participants already enjoyed the option in 2014. Today, QR codes are used not for merely informative purposes: Kleiner Perkins Caufield & Byers, Visa Inc., and GfK reports 4% of the global consumer transactions are via QR code. China got literally obsessed with payment option. ‘The Chinese scan QR codes to make payments, get information, authenticate themselves, avail offers, and for practically every other use case’ (Scanova). CNN tech reported $1.65 tr in transactions via QR codes in China for 2016.

How banks are going to compete

It’s unlikely that banks will retain the hegemony in the money transfer and payment market. However, in order not to lose what’s left to them, there’s an urgent need for the banking system to adopt new top-notch tech solutions. What software application developers propose for the banks to help them follow the scenario of digital disruption?

Considering our affinity to mobile devices, software developers see mobile banking as one of the strongest tools for a bank to keep the existing and attract new clients. According to the PwC’s 2018 Digital Banking Consumer Survey, online dominant consumers are becoming mobile consumers. The survey showed that 15% of the consumers are now using largely their mobile to get almost any banking service. ‘To a growing number of consumers, banking just is a mobile activity’. Moreover, a study conducted by City Mobile in 2018 states that mobile banking is among top three apps most commonly used by Americans. As we see, the population still highly trusts the banks. The latter in their turn must seize the moment with a launch of a decently-arranged mobile banking. This will bring additional value for the users along with the new profits for the banks. So, what are the features a custom software developer may introduce to launch a customer-centric tech asset? See the full list of them based on the capabilities of Standfore banking platform by Qulix System.

- Payments and transfers

Today’s mobile banking is a one-fits-all solution to effect payments, perform P2P, A2A and other transfers, send and receive invoices. This powerful tool allows exchanging currency, viewing user’s transactions history and generating analytical reports for bank employees.

- Notifications

Banks now want informative SMS/PUSH notifications for their clients. To be even closer, they make use of Viber / WhatsApp integration capabilities.

- My finances

With this feature, banks’ clients are now able to easily manage their e‑wallets, accounts, statements, alongside deposit and credit cards. Options are also available for monitoring client’s loans, deposits, metal accounts and safe boxes. Banks don’t underestimate free stuff: with the right platform at their hands, they offer their clients loyalty bonuses and gift cards or other items at their discretion.

- Open zone

Banks are improving their market presence by providing services for non-clients who can log in with simplified authentication.

- Social

Modern banks are more responsive and help their clients share their positive experiences with friends via social networks. Funds can now be transferred easily due to introducing P2P and crowd-funding features.

- Geo-targeting

Clients have no trouble locating an office due to an ATM/Branch locator. Best places and prices are now available to banks’ clients thanks to geo-targeting capabilities. Special offers from the partners help banks create truly exceptional experience for their clients.

Banks are not going to give in in this battle for loyalty, as they are ready and eager to fight for their technical supremacy over non-banking institutions. Being actively involved in the development of the sector, Qulix Systems is observing a huge demand for custom development services here. The dawn of digital banking is long past, now it is rather a broad day than anything else.

Want more expertise from a mature web and mobile application developer? Visit our page for more information on our products or go directly to Standfore page.

Contacts

Feel free to get in touch with us! Use this contact form for an ASAP response.

Call us at +44 781 135 1374

E-mail us at request@qulix.com

Feel free to get in touch with us! Use this contact form for an ASAP response.

Call us at +44 781 135 1374

E-mail us at request@qulix.com

![]()

![]()

![]()