Digital wallet platforms today process 50% of e-commerce payments worldwide, and this figure will grow further. At the same time, the number of fraud cases is growing, regulatory authorities are increasing the volume of requirements and introducing new initiatives, such as the European CESOP, the updated PCI DSS v4.0, and eIDAS 2.0. The market demands a digital wallet that takes into account the requirements of security, transparency, and regulatory control by default.

Our e-wallets and other fintech solutions are built on the principle of compliance by design. This means that we build compliance into architecture. In this article, we will tell you how our security architecture is structured, what processes help us stay one step ahead, and how we form a culture of trust — from design to daily support of our customers and regulators.

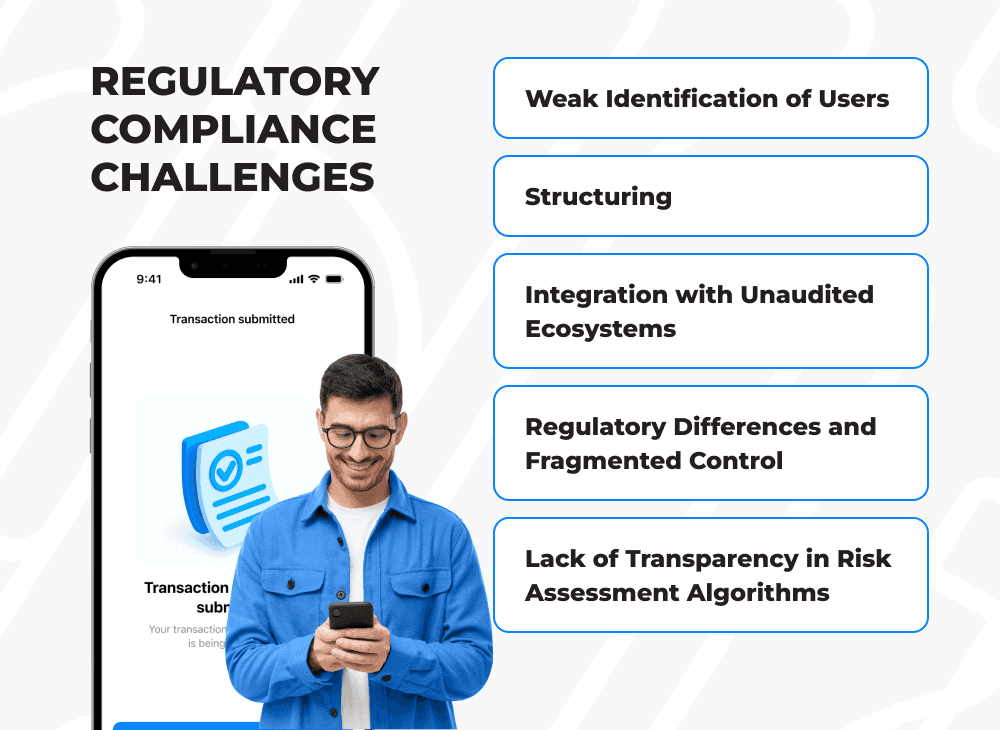

Mobile Wallets in 2026: Regulatory Compliance Challenges

Millions of people use digital wallets to conveniently and securely send money, make purchases, store payment cards, discount coupons and tickets, manage expenses, as well as connect to transport systems and fintech apps. Users make mobile payments by QR codes, track their costs and revenues through transaction history, accumulate bonuses via integrated loyalty programs, and, in general, appreciate the opportunity to leave cash at home.

There are a lot of mobile wallets in the market, from top Apple Pay and Google Pay to unknown ones. They are different, but all of them have two identical goals. The first one is to deliver more unique features to provide customers with seamless experience and convenience, and the second one is to meet the regulatory requirements for data and fraud protection. However, the European Banking Authority's report found that many payment services have disproportionately weak AML controls compared to the level of threats.

High speed of transactions and wide availability make mobile wallets vulnerable. These risks include:

Weak Identification of Users

Many mobile wallets allow customers to register in minutes using only a phone number or email. The lack of strict KYC (Know Your Customer) procedures and the unavailability of biometric verification opens up opportunities for attackers, especially when dealing with cross-border transactions or cryptocurrency. This makes it difficult to establish the true identity of the user and makes the digital wallet vulnerable to fraudulent schemes, money laundering, and terrorist use.

Structuring

A single large transaction is split into a series of smaller transfers to bypass thresholds at which financial institutions are required to conduct additional checks and submit reports (e.g., AML/CFT). Criminals use mobile wallets with high availability and automation because it’s easy to break up large sums especially if transaction limits are flexible enough.

Integration with Unaudited Ecosystems

Modern e-wallets are increasingly integrating with crowdfunding platforms, NFTs, play-to-earn games, and other unaudited digital ecosystems. These connections allow participants to move money between sectors that may be outside the scope of traditional financial regulation on their own. Without end-to-end monitoring and uniform reporting standards, these integrations pose significant risks to transparency and control.

Regulatory Differences and Fragmented Control

Compliance teams have to meet dozens of regulatory requirements in different countries. With some jurisdictions tightening controls while others lag in implementing AML/CTF standards, the phenomenon of regulatory arbitrage is emerging — the relocation of operations to countries with less stringent rules. The lack of global harmonization of regulations requires digital wallets to have a flexible architecture for managing compliance policies and adapting to rapidly changing requirements.

Lack of Transparency in Risk Assessment Algorithms

Digital wallets actively use artificial intelligence and machine learning for transaction monitoring and behavioral scoring. Nevertheless, regulators are increasingly demanding explainable AI — the ability to explain why the algorithm made a certain decision about the suspiciousness of a transaction. Without clear logic, the model can be considered invalid, especially in the context of litigation and investigations. This makes it critical to implement transparent and verifiable risk management mechanisms.

Regulatory Landscape for e-Wallets

Regulators developed a series of laws to make mobile payments secure and transparent, as well as to protect customers' data. The key regulations include:

What Is a Compliant Digital Wallet?

CoinLaw found that 5% of crypto wallets were compromised because of integration vulnerabilities. By the way, $1.2 billion was spent to improve security issues, including encryption technologies. Let’s see how regulators define a proper mobile wallet:

Secure

A mobile wallet must ensure data and transaction protection at all levels, from storing personal information to transmitting payment details. Regulators require developers to implement up-to-date cryptographic mechanisms, a robust infrastructure, as well as multi-factor authentication that can protect customers from unauthorized access.

AML/KYC-compliant

The platform should effectively identify customers, track transactions in real time, and generate reports on suspicious transactions. The digital wallet must be able to respond to potential threats and interact with regulatory authorities transparently and promptly.

Be licensed

The mobile wallet must operate within a clearly defined legal model. Developers should obtain the appropriate permissions and specify the jurisdiction in the user documents. Without legal status, the platform will be beyond the scope of trust and can be blocked by regulators.

User-Centric in Regulatory Protection

The digital wallet must protect consumer rights, including transparency of terms (fees, limits, refunds, etc.), the implementation of dispute resolution mechanisms, and others. Customers would like to feel that the platform is not only convenient but also reliable.

Data Protection-Compliant

The mobile wallet should collect personal information strictly with the consent of consumers and store it in compliance with the principles of minimization and privacy-by-design. Customers have the right to control their data, including the ability to transfer or delete it, which is especially important in the context of growing attention to digital ethics.

Be Scalable and Interoperable

The digital wallet should be ready to integrate with banking and fintech systems, support open APIs, and comply with the requirements of different jurisdictions. Its architecture should provide for easy localization of legal texts and validation procedures. Such flexibility guarantees the businesses sustainability and global growth.

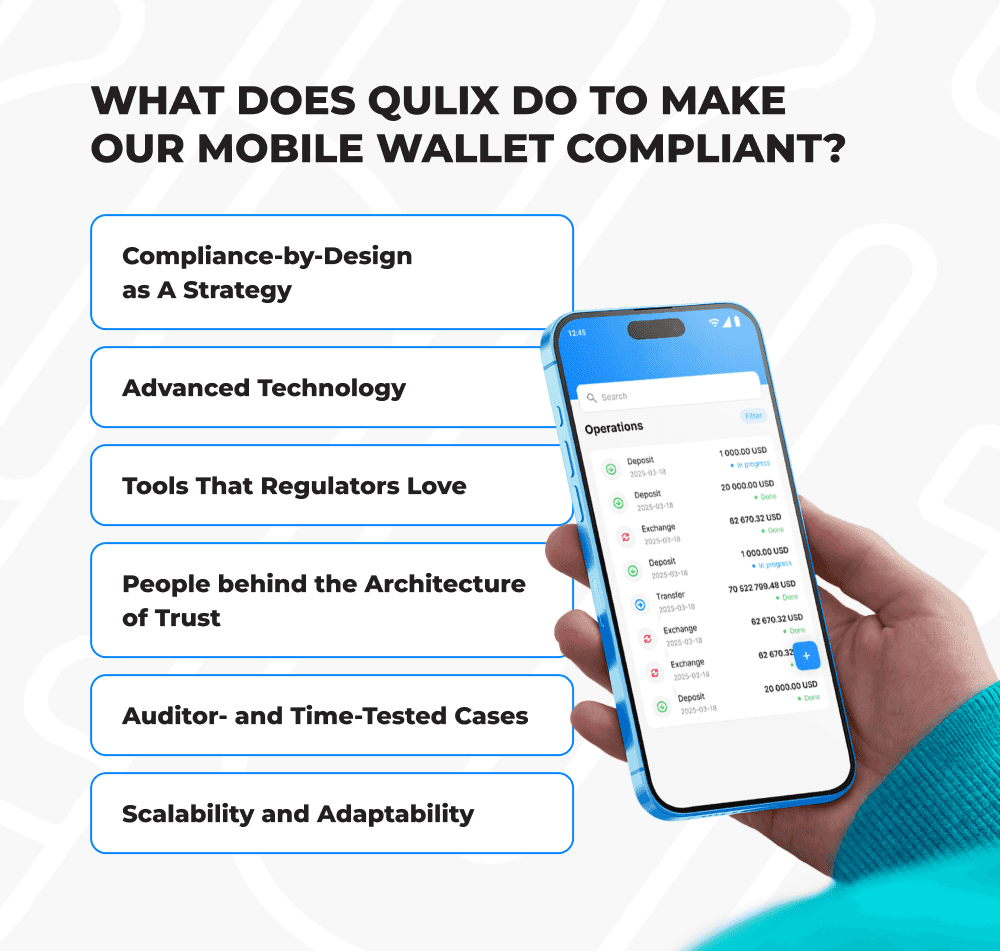

What Does Qulix Do to Make Our Mobile Wallet Compliant?

Our company has been specializing in the development of fintech applications and digital wallets for over 20 years, and this experience has allowed us not only to adapt to constantly changing regulatory requirements, but also to form our own standards within the industry. What do we do to ensure that our web platform meets all compliance and regulatory requirements?

Compliance-by-Design as A Strategy

We design our fintech solutions from the start with AML/CFT, GDPR, and other standards in mind. The compliance requirements are built-in at the technical design level. We take into account the principles of data transparency, traceability, and verifiability even before writing the first lines of code. This approach allows our digital wallet not only to comply with regulations, but also to scale without losing compliance when entering new markets.

Advanced Technology

Our mobile wallet is built on a microservice architecture with containerization that allows us to quickly scale the digital payment platform as the load increases. We use the Zero Trust approach, end-to-end encryption, and an integrated real-time risk assessment system. Each transaction is analyzed by patterns, such as origin of funds, frequency of actions, geography, time of day, etc. They allow us to create a dynamic risk profile of the user and preventive protection against potential crime.

Tools That Regulators Love

We have developed built-in reports that comply with FATF, GDPR, and ISO 27001. The automatic logging system records all important user and administrator actions, including changes to security settings, login attempts, and withdrawal requests. Our API allows us to integrate with regulatory portals and configure data export in XML or JSON format taking into account the requirements of local supervisory authorities. This helps us eliminate manual work and accelerate audit processes.

People behind the Architecture of Trust

Our mobile wallet is run by our highly-qualified and experienced employees. Architects with a banking background and developers design a scalable infrastructure, compliance specialists ensure compliance, security engineers implement protection, and UX/UI designers and product managers create a user-friendly and controllably transparent interface. This approach allows us to release a product that fully meets international standards and the expectations of regulators around the world.

Auditor- and Time-Tested Cases

We have already developed and implemented a lot of fintech solutions. Our partners note that using our mobile wallet simplifies preparation for external audits, increases transparency for investors, and allows for faster legal approvals. This is not just a fintech tool, it is a strategic asset for business.

Support for International and Regional Regulations

We implement an architecture that allows us to flexibly customize AML, KYC, data protection, and reporting rules to the requirements of a specific jurisdiction. This includes localization of legal texts, consent templates, trigger thresholds, and reporting formats. Thus, our mobile wallet platform complies with the regulations of the EU, USA, MENA, and other regions without the need to rewrite the code.

Scalability and Adaptability

Our digital wallet is:

As your business operations grow, compliance does not become an obstacle, it becomes a guide.

Last Word

Our goal is not to meet the minimum requirements, but to exceed them. Our mobile wallet is the result of multidisciplinary work, strategic thinking, and technological expertise. It helps compliance teams do their job better, gives confidence to regulators, and strengthens users' trust in our brand.

We are ready to show you how it works: order a demo, discuss cases, or provide a technical whitepaper. Qulix is building not just a platform for transactions, we are building an open-source mobile wallet platform of trust.

Related articles

About the Author