In fintech, launching a digital wallet seems like a logical step, whether you’re a startup looking to change the industry or a mature company expanding its ecosystem. According to Statista, the global digital payment market is projected to reach nearly $27 trillion in 2026. With an e-wallet, your business can enhance customer experience, expand into new markets, and gain greater control over user data.

Before your developers write the first line of code, it’s important to understand that a digital wallet is more than just an app. It’s a complex, regulated product that affects user safety, compliance, and trust in your brand. Companies that decide to develop a mobile wallet themselves often face delays, fines, and technical issues that could have been avoided by turning to professionals.

Our new blog article is a step-by-step guide that will help you avoid common mistakes, build a competitive advantage, and lay the foundation for a scalable product.

Common Mistakes Made by Companies Developing a Mobile Wallet on Their Own

Sometimes businesses try to develop a digital wallet by themselves, without turning to specialists, and make the following mistakes:

1. Underestimating Regulatory Requirements

Digital wallet platforms operate in one of the most strictly regulated areas — financial services. KYC/AML, GDPR, PCI DSS, licenses, and other regulations are not just formalities but mandatory elements of the architecture.

What goes wrong:

Why it matters: Violating the law means fines, blocking, and loss of reputation. A digital wallet is not just code; it’s a financial instrument that must be legally impeccable.

2. Errors in Security Architecture

Security is not a feature; it is the basis of trust. Some development teams believe that standard encryption is enough and miss critical aspects of protection.

What goes wrong:

Why it matters: One incident will cost you user trust. Security should be built in from day one and not added on the fly.

3. Development Without Scalability In Mind

A digital wallet is not a static product. It should support new currencies, integrations, countries, and features.

What goes wrong:

Why it matters: If a mobile wallet doesn’t grow with the business, it’s holding back the development process. Flexibility and scalability are the keys to long-term success.

4. Ignoring UX and Accessibility

User experience determines the success of the e-wallet. But in-house teams often focus on backend logic, forgetting about simplicity, accessibility, and localization.

What goes wrong:

Why it matters: Bad UX leads to user churn. Trust and convenience go hand in hand in fintech.

5. Difficulties With Integrations

A digital wallet doesn’t exist in a vacuum. It should integrate with payment gateways, banks, identity providers, and other systems.

What goes wrong:

Why it matters: The mobile wallet won’t exist without reliable integrations. It should be part of an ecosystem. Don’t create an isolated solution.

How to Create a Successful Digital Wallet: Where to Start?

Now, it’s time to find out what to do to build a reliable digital wallet platform and avoid the above-mentioned mistakes.

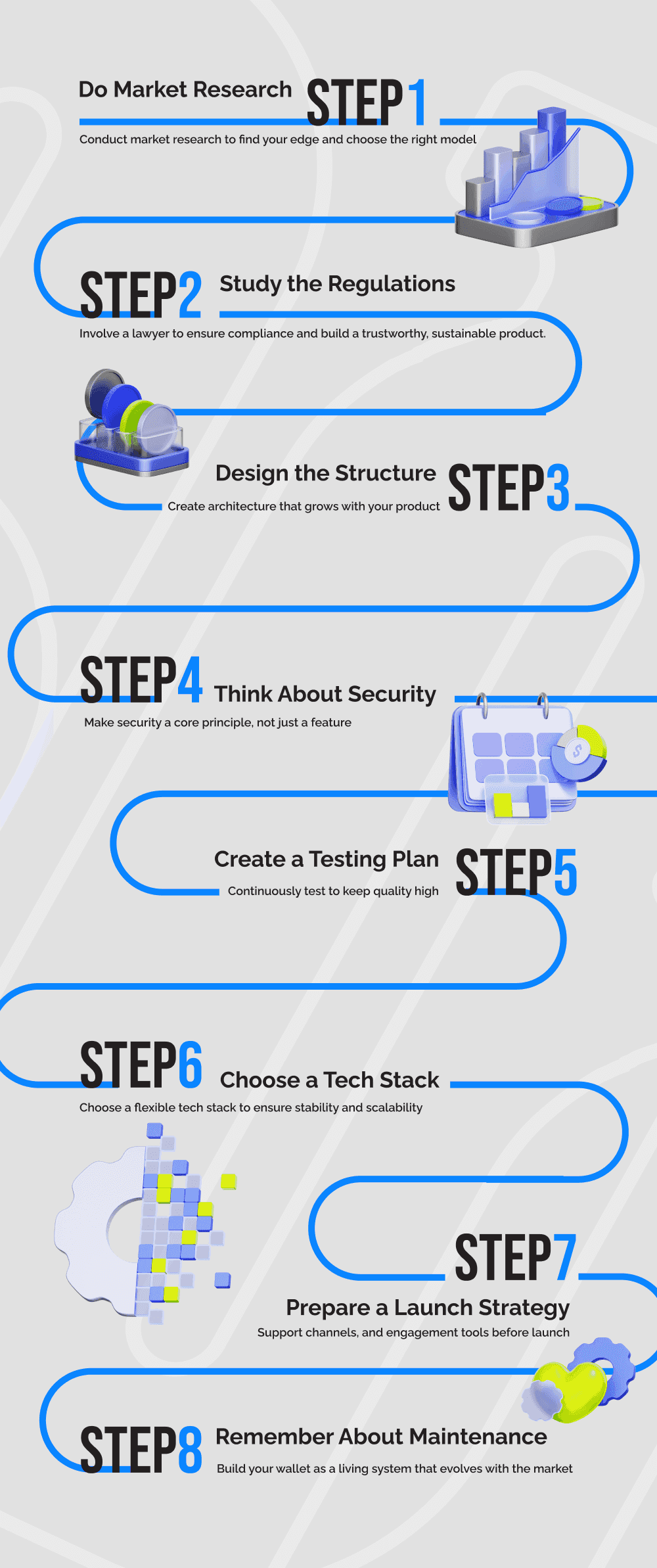

Step 1: Do Market Research

First of all, research the digital wallet market, identify the main competitors, their advantages and disadvantages. Capital One Shopping revealed that the most popular mobile wallets include Google Pay (56% of users), Apple Pay (53%), and Samsung Pay (52%). You should also understand what purpose your app will serve. Be able to answer the following questions:

For example, if you are targeting an emerging market where banking infrastructure is limited, your e-wallet can become a financial inclusion tool. And if you are launching a product for a younger audience, it may be worth integrating gamification, tokenization, or cryptocurrency support.

Conduct a competitive analysis and determine what types of wallets already exist:

This will help you formulate a unique value proposition and choose the right business model.

Step 2: Study the Regulations

Fintech is one of the most regulated industries, and ignoring the legal aspects can lead to serious consequences. Carefully study the requirements for personal data protection, anti-money laundering, payment information security, and licensing. Depending on the region where you plan to launch your digital wallet platform, the rules can vary greatly. For instance, Europe has PSD2 and GDPR directives, the USA has its own standards, and MENA countries often require partnerships with local banks.

At this stage, it will be good to involve a lawyer specializing in fintech to help you determine whether a license is needed, what documents are required for KYC/AML, and how to integrate legal requirements into the app architecture. This is not just a formality; it’s the basis of trust and sustainability of your business.

Step 3. Design the Structure of the Mobile Wallet and MVP

One of the most common mistakes is trying to create everything at once. Instead, you should start with a minimum viable product (MVP) that solves one key user problem. This could be a simple e-wallet for storing payment cards and paying via QR code. It’s important to determine which features will be basic and which can be added later.

At the MVP stage, we recommend you focus on the following features: registration, authorization, depositing and withdrawal of funds, transaction history, and integration with banking APIs. Additional features like cashback, multi-currency, cryptocurrencies, or expense analytics can be implemented later. The main thing is to build the architecture in such a way that it allows for scaling and adding new features without a complete redesign.

Step 4. Think About Security

Security is not just a set of features but a philosophy that should be built into every layer of the digital wallet. Financial applications work with sensitive data, and any vulnerability can lead to a loss of trust, fines, and reputational risks. Therefore, take into account data encryption, API protection, tokenization, two-factor authentication, and regular audits.

Your task is to protect user data and explain to customers how you do it. Transparency in security issues increases trust and reduces barriers to registration. Besides, it’s worth implementing mechanisms for detecting fraud and abnormal behavior to respond to threats in real time.

Step 5. Create a Testing Plan

Financial apps don’t forgive mistakes. Gen Z users expect flawless performance and easily switch platforms in case of even minor glitches. Therefore, testing should be an ongoing process. You need to check your mobile wallet for functionality, security, performance, and compatibility with different platforms.

Particular attention should be paid to load testing to ensure that the application can withstand the growth of users. We recommend you test the UX, too. Check how convenient it is to use the digital wallet, how clear the interface is, and how quickly the user can make a transaction. Using CI/CD, automated tests, and monitoring will help you maintain high quality at all stages.

Step 6. Choose a Tech Stack

Selecting the right tech stack determines not only the speed of the development process but also the stability, flexibility, and scalability of the product. Frontend developers use React Native or Flutter because they allow them to create cross-platform applications. Backend teams often work with Node.js, Python, or NestJS. PostgreSQL and Redis are used for databases, and AWS, Docker, and Kubernetes are chosen for cloud infrastructure.

Bear in mind the possibility of integrating your app with blockchain or making it compatible with IoT. A flexible architecture will allow you to quickly adapt to new requirements and markets.

Step 7. Prepare a Launch Strategy

Launching is not just publishing your digital wallet on the App Store. It’s a time when you enter the market, and it determines how users will meet you. Prepare a marketing strategy, support channels, training materials, and feedback mechanisms in advance. Collect feedback and make improvements. Include referral programs, registration bonuses, and partner integrations. All this will help you seamlessly release the app and create a community around it.

Step 8. Remember About Maintenance

A digital wallet is a platform that should be constantly evolving. After launch, you must collect feedback, analyze user behavior, and release updates regularly. This includes adding new features, supporting new currencies, entering new markets, or improving UX. Using analytics, A/B testing, and machine learning models will help you make decisions based on data. Perceive your digital wallet as a living system that must adapt to changing market conditions.

Why Is It Better to Go to Professionals?

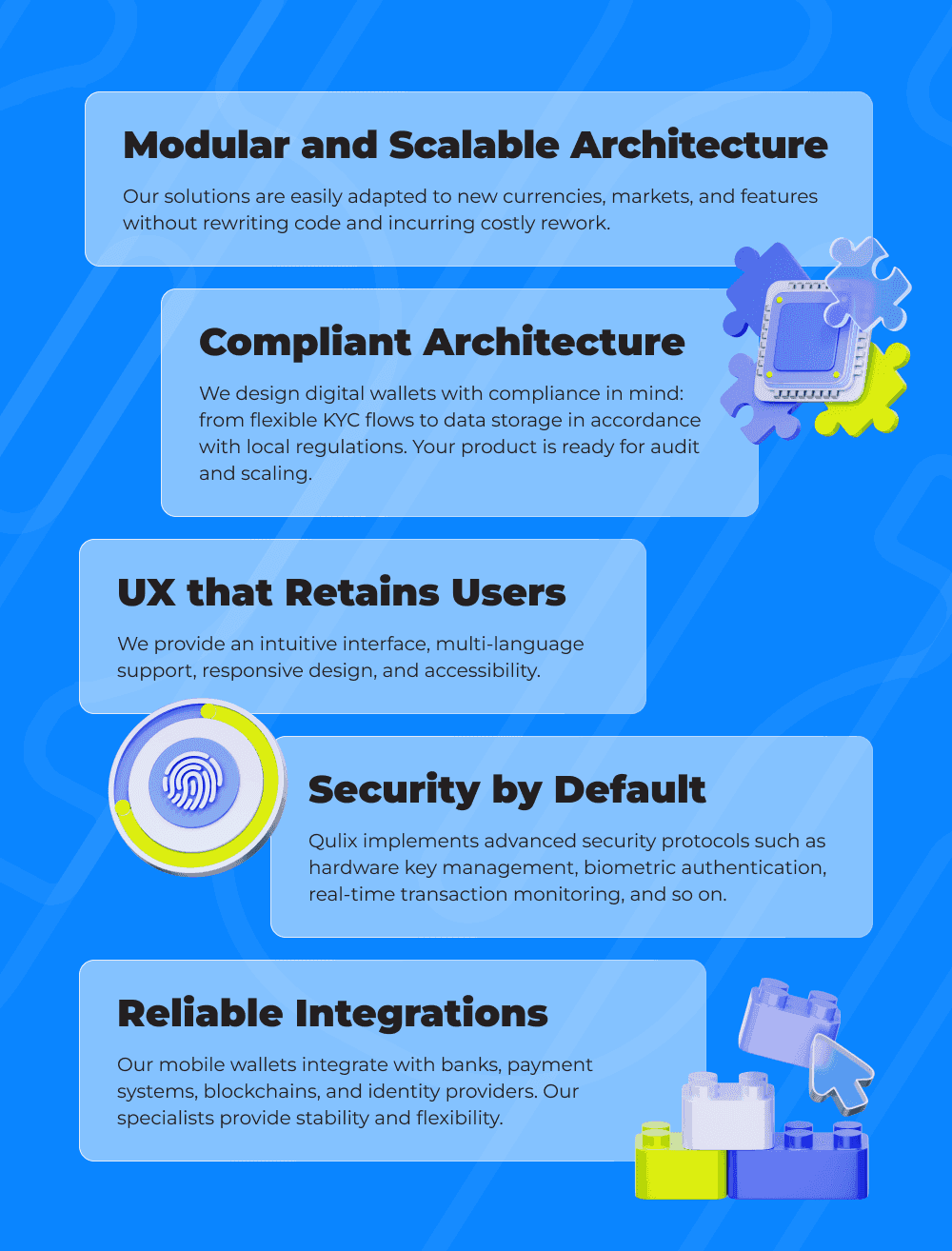

Qulix specializes in developing white-label e-wallets that meet security, scalability, and compliance requirements from day one. We offer:

Compliant Architecture

We design digital wallets with compliance in mind: from flexible KYC flows to data storage in accordance with local regulations. Your product is ready for audit and scaling.

Modular and Scalable Architecture

Our solutions are easily adapted to new currencies, markets, and features without rewriting code and incurring costly rework.

Security by Default

Qulix implements advanced security protocols such as hardware key management, biometric authentication, real-time transaction monitoring, and so on.

UX that Retains Users

We provide an intuitive interface, multi-language support, responsive design, and accessibility.

Reliable Integrations

Our mobile wallets integrate with banks, payment systems, blockchains, and identity providers. Our specialists provide stability and flexibility.

Case studies: What Our Clients Managed to Avoid

Last Word

Launching a digital wallet is more than just a technical project. It’s a strategic decision that will determine the future of your product. Mistakes at the start can cost you dearly — both in money and reputation. By turning to a professional team that understands fintech, security, compliance, and UX, you’re not just getting development — you’re getting a solid foundation for growth.

Ready to discuss your project? We’ll help you build a mobile wallet that people trust.

Related articles

About the Author